[Infographic] 10 Pieces of Retirement Planning Advice Retirees Wish They Had Known Sooner

Planning for a secure financial future isn’t always rosy. There are dozens of threats along the way that can derail a happy retirement. But it is important to understand that with the proper preparation, the right guidance, and a little know-how, you can significantly improve your odds of reaching your retirement goals safely.

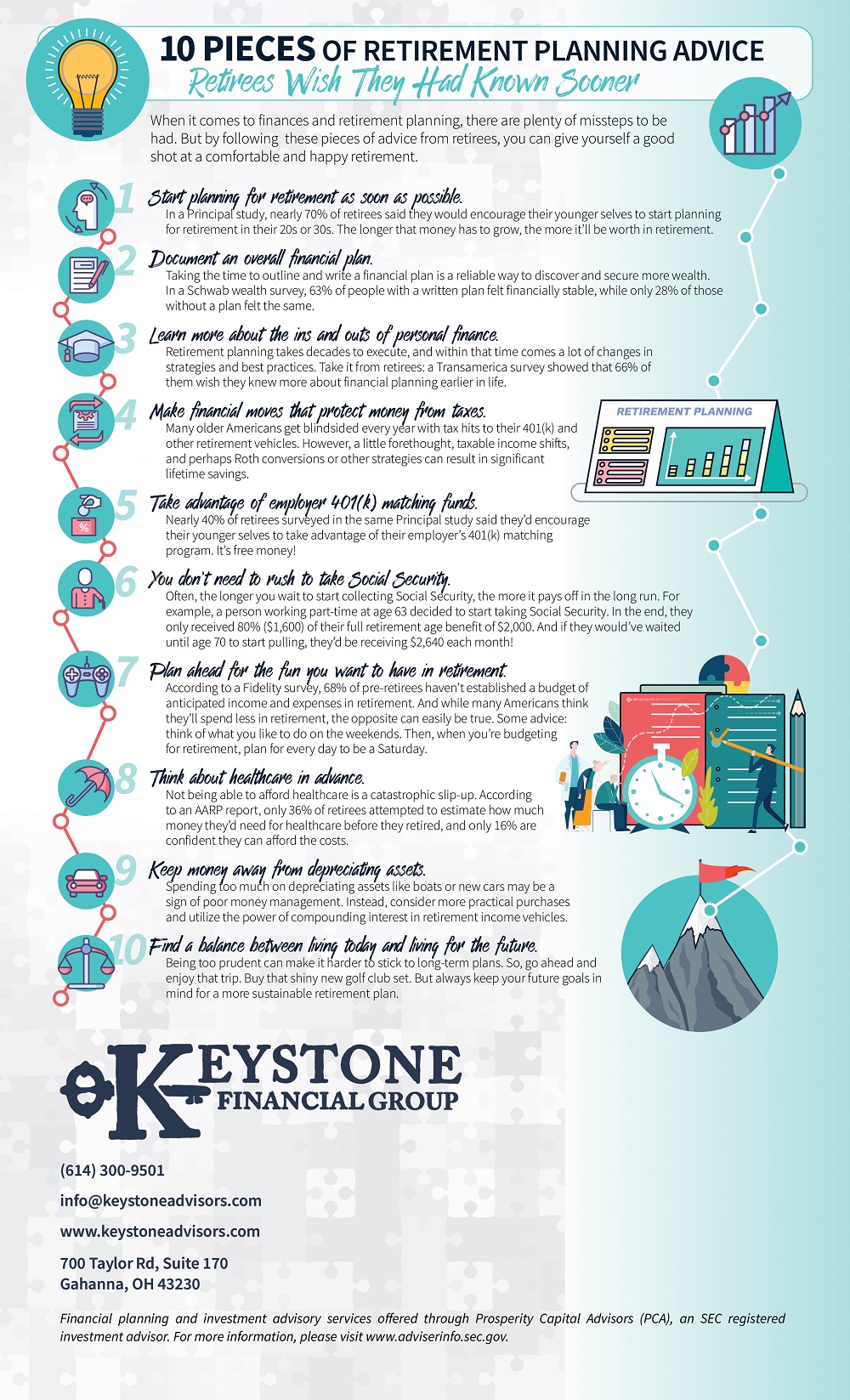

Check out our new infographic, 10 Pieces of Retirement Planning Advice Retirees Wish They Had Known Sooner, to learn from those who have been in your shoes on how to avoid common retirement planning missteps. Here are 10 things current retirees think you should know:

1. Start Planning Early

In a Principal study, nearly 70% of retirees said they would encourage their younger selves to start planning for retirement in their 20s or 30s.1 The longer that money has to grow, the more it’ll be worth in retirement.

2. Define Your Plan

Taking the time to outline and write a financial plan is a reliable way to discover and secure more wealth. In a Schwab wealth survey, 63% of people with a written plan felt financially stable, while only 28% of those without a plan felt the same.2

3. Improve Your Financial Literacy

Retirement planning takes decades to execute, and within that time comes a lot of changes in strategies and best practices. Take it from retirees: a Transamerica survey showed that 66% of them wish they knew more about financial planning earlier in life.3

4. Implement Tax Planning Strategies

Many older Americans get blindsided every year with tax hits to their 401(k) and other retirement vehicles. However, a little forethought, taxable income shifts, and taking advantage of Roth conversions or other tax-saving strategies can result in significant lifetime savings.

5. Take Advantage of Employer 401(k) Matching Funds

Nearly 40% of retirees surveyed in the same Principal study said they’d encourage their younger selves to take advantage of their employer’s 401(k) matching program. After all, it’s free money!

6. Don't Rush to Take Social Security

Often, the longer you wait to start collecting Social Security, the more it pays off in the long run. For example, a person working part-time at age 63 decided to start taking Social Security. In the end, they only received 80% ($1,600) of their full retirement age benefit of $2,000. And if they would’ve waited until age 70 to start pulling, they’d be receiving $2,640 each month!

While it's not always appropriate to delay filing until 70, there are many cases where this can make a huge difference to your retirement income - and to your spouse's future financial security, should you pass away first. Consult with a qualified Social Security planning specialist to determine which filing strategy is best for your situation.

7. Create a Retirement Budget

According to a Fidelity survey, 68% of pre-retirees haven’t established a budget of anticipated income and expenses in retirement.4 And while many Americans think they’ll spend less in retirement, the opposite can easily be true. Some advice: think of what you like to do on the weekends. Then, when you’re budgeting for retirement, plan for every day to be a Saturday.

8. Plan for Healthcare Needs

Not being able to afford healthcare is a catastrophic slip-up. According to an AARP report, only 36% of retirees attempted to estimate how much money they’d need for healthcare before they retired, and only 16% are confident they can afford the costs.5 Long-term care costs can quickly eat away at your retirement savings if you don't plan properly.

9. Limit Depreciating Assets

Spending too much on depreciating assets like boats or new cars may be a sign of poor money management. Instead, consider more practical purchases and utilize the power of compounding interest in retirement income vehicles.

10. Find a Balance

Being too prudent can make it harder to stick to long-term plans. So, go ahead and enjoy that trip! Buy that shiny new golf club set. But always keep your future goals in mind for a more sustainable retirement plan that will last as long as you do.

Sources:

https://www.schwab.com/resource-center/insights/content/does-financial-planning-help

https://www.moneytalksnews.com/6-important-things-to-do-before-retirement/

https://www.aarp.org/research/topics/health/info-2014/2013-Health-Care-Costs-Survey/

Disclaimer:

This content is developed from sources believed to be providing accurate information. The information provided is not written or intended as tax or legal advice and may not be relied on for purposes of avoiding any Federal tax penalties. Individuals are encouraged to seek advice from their own tax or legal counsel. Individuals involved in the estate planning process should work with an estate planning team, including their own personal legal or tax counsel. Neither the information presented nor any opinion expressed constitutes a representation by us of a specific investment or the purchase or sale of any securities.